Survey Experts · 07.01.2026 · 32min read

In honor of Financial Literacy Month, the Appinio Hype Tracker Report explored the various financial products and services available to consumers and examined the state of finance and digital banking in the US.

In this article, we summarize the report's key findings, providing a closer look at:

- The importance of financial literacy and its current state in the US

- Various financial products available, including:

- savings accounts

- investment options

- retirement planning products

- insurance products

- cryptocurrency

- Benefits of digital banking and offers that could win banks new American customers

- What Americans are currently saving for.

💡Want to see the results at glance? Then download the Appinio Hype Tracker Report for free.

Financial literacy in the US

April is Financial Literacy Month, a time when individuals and organizations focus on promoting financial education and awareness.

Financial literacy is critical in helping individuals make informed decisions about managing their money. As the financial landscape becomes increasingly complex, having a solid understanding of basic financial concepts is essential to making informed choices regarding investments, savings, credit, and debt management.

Without financial literacy, individuals may not fully comprehend the implications of their financial decisions, leading to poor choices that can adversely affect their financial stability and future.

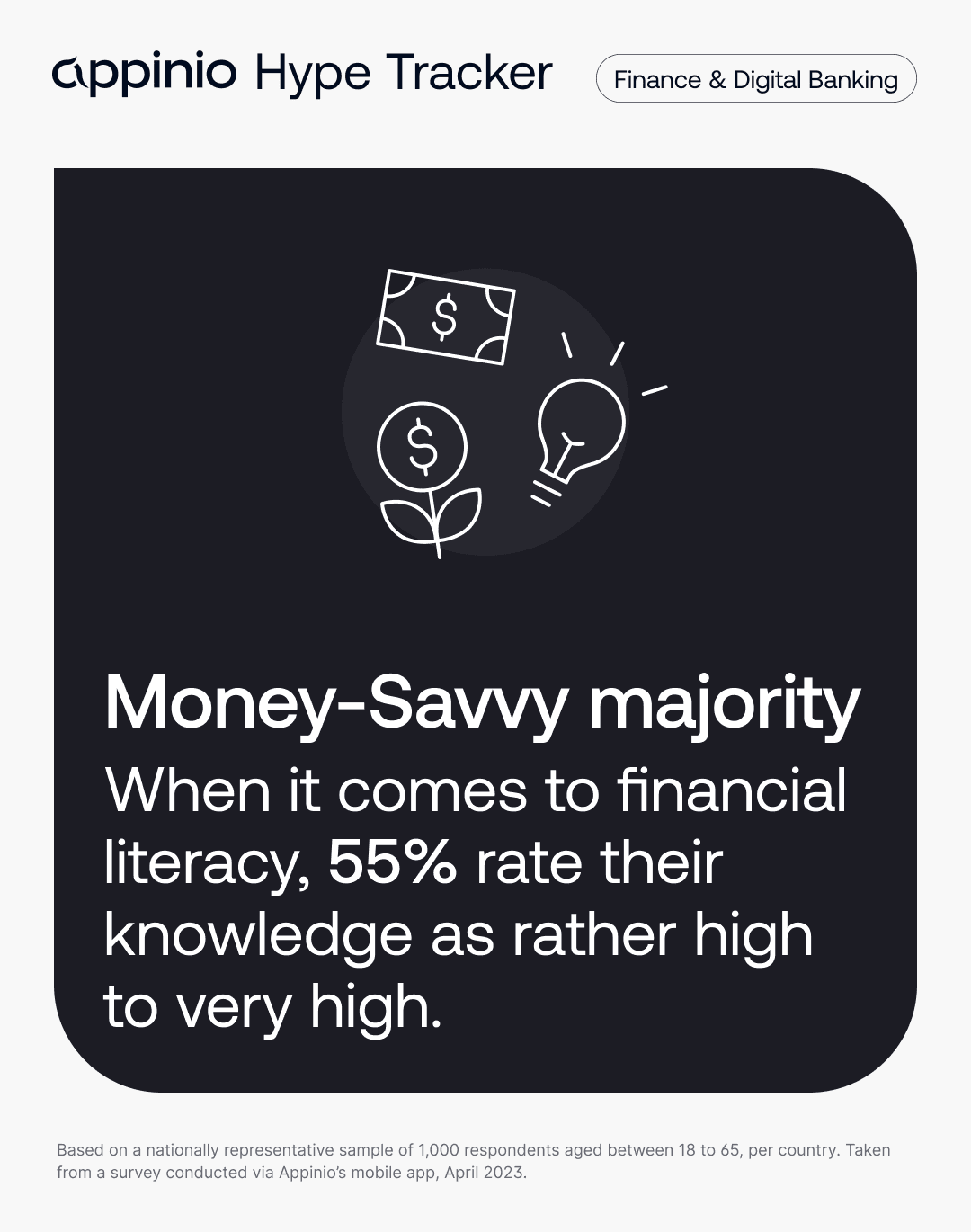

According to the Appinio Hype Tracker Report, 55% of Americans rate their financial knowledge as rather high to very high. This level of confidence in understanding finance, financial products, and financial decisions by over half of Americans is not surprising, considering that at least 47% of respondents reported earning over $50,000 annual household disposable income.

However, it's crucial to have a basic understanding of different financial products such as savings accounts, investments, retirement planning options, credit scores, budgeting, debt management, and insurance. By improving financial literacy and understanding these concepts, individuals can make better financial decisions, secure better loan terms, and lower interest rates, ultimately improving their overall financial wellbeing.

Financial products: which ones do Americans hold?

There are a variety of financial products available in the US that can help people achieve their financial goals.Here are some of the most popular options in the US:

- Savings accounts

These accounts offer a low-risk way to earn interest on the money saved. They're an ideal option for short-term savings goals, emergency funds, or saving up for a larger purchase. Almost one in two Americans (47%) hold a savings account. - Investment products

Investment products may be a good option when looking for higher potential returns. Some popular options include:

- Stocks

Buying a stock, means buying a small piece of ownership in a company. Stocks can offer high potential returns, but also come with higher risk.

The value of a stock can go up or down based on various factors such as the company's performance, industry trends, or economic conditions. Investors can profit from stocks by buying low and selling high, or through dividends paid out by the company to its shareholders. Findings from our Hype Tracker report found that over one in four Americans (28%) own stocks. - Bonds

Bonds are debt securities issued by companies or governments as a means of borrowing money. When you purchase a bond, you are essentially loaning money to the issuer in exchange for periodic interest payments and the return of your principal investment when the bond matures. Bonds are generally considered less risky than stocks and can provide a steady stream of income for investors. - Managed funds

Also called mutual funds or collective investment schemes, are portfolios of diversified investments managed by a professional fund manager on behalf of individual investors. These funds allow investors to access a diversified mix of investments that may be difficult to achieve on their own, and investors purchase units or shares that reflect the underlying value of the assets held by the fund. Our survey shows that 17% of American respondents say they hold managed funds. - ETFs

ETFs, or exchange-traded funds, are investment funds that trade on stock exchanges like individual stocks. ETFs are typically designed to track the performance of a particular index, such as the S&P 500, and are made up of a basket of assets, such as stocks or bonds, that mimic the composition of the index. ETFs provide investors with an easy way to gain exposure to a wide range of assets at a lower cost than buying each asset individually. Additionally, ETFs can be bought and sold throughout the trading day, providing investors with more flexibility than traditional mutual funds. Over one in ten (13%) of US respondents reported investing in ETFs. - Cryptocurrencies

Cryptocurrencies are digital or virtual currencies that use cryptography for security and operate independently of a central bank. Unlike traditional currencies, which are issued and controlled by a government, cryptocurrencies use decentralized technology, such as blockchain, to manage and record transactions. Cryptocurrencies have gained popularity among investors due to their potential for high returns and the relative anonymity they provide. However, they are also highly volatile and their value can fluctuate rapidly. Cryptocurrencies are held by nearly a quarter (22%) of US respondents.

- Stocks

- Retirement planning products

Retirement planning is a crucial aspect of personal finance, and having a retirement plan in place can significantly impact one's financial wellbeing in their golden years. In the US, there are several retirement planning products available to individuals, including Individual Retirement Accounts (IRAs), 401(k)s, and annuities.

Our study found that 13% of Americans have invested in private pension plans.- Individual Retirement Accounts (IRAs)

IRAs are retirement savings accounts that individuals can open on their own. There are two primary types of IRAs, traditional and Roth. With a traditional IRA, contributions are tax-deductible, and taxes are paid when funds are withdrawn during retirement. Roth IRAs, on the other hand, have contributions made with after-tax dollars, but withdrawals during retirement are tax-free. - 401(k)s

401(k)s are employer-sponsored retirement plans that allow employees to contribute a portion of their pre-tax income towards retirement savings. Many employers offer matching contributions up to a certain amount, which can significantly boost an employee's retirement savings. Unlike IRAs, 401(k)s have contribution limits and may have fees associated with them. - Annuities

Annuities are a type of retirement investment product that offers a guaranteed income stream for life or a set period. In the US, annuities are primarily sold by insurance companies and can be classified into two main types: immediate and deferred annuities. Immediate annuities require a lump sum payment and provide income immediately, while deferred annuities allow individuals to make payments over time and begin payouts at a later date.

Annuities can offer tax advantages and act as a hedge against market volatility, but they also come with fees and potential limitations. It's important to carefully consider an annuity's terms and conditions before making an investment decision.

- Individual Retirement Accounts (IRAs)

- Insurance products

Our study found that nearly one-fifth of Americans (18%) have invested in insurance products. Some common types of insurance include:- Health insurance

Covers medical expenses and treatments. - Car insurance

Covers damage to your vehicle and liability in the event of an accident. - Life insurance

Provides a payout to your beneficiaries in the event of your death. - Homeowners/renters insurance

Protects your property and possessions in the event of damage or theft.

- Health insurance

- Portfolio management tools

These are tools and services that can help people manage their investments and financial planning goals. Some popular options include robo-advisors, which use algorithms to create and manage a diversified investment portfolio.

By understanding the different financial products available, individuals can make informed decisions that align with their financial planning goals.

Appinio Hype Tracker report: Financial products owned by Americans

According to our survey, here are some key highlights of financial products owned by Americans:- Almost one in two Americans (47%) hold a savings account.

- Over one in four Americans (28%) own stocks.

- 17% of American respondents say they hold managed funds.

- Over one in ten (13%) of US respondents reported investing in ETFs.

- Cryptocurrencies are held by nearly a quarter (22%) of US respondents.

- 13% of Americans have invested in private pension plans.

- Nearly one-fifth of Americans (18%) have invested in insurance products.

💡Want to deep dive into what US consumers think of Cryptocurrencies, NFTs and other investment products?

We have a spotlight for that! Download the Investment Appinio Spotlight and satisfy your curiosity!

How Americans inform themselves on financial products

The Appinio Hype Tracker Report shows that 37% of Americans turn to loved ones like friends and family members for advice on financial products, while 32% rely on investment platforms, and 29% use financial advisors to inform themselves about financial products.

Surprisingly, more than one-third of Americans (34%) rely on YouTube for financial advice, while nearly one-third (30%) turn to other social media platforms.

American Gen X’s guide to finance

Among the younger generation, Gen X is most likely to turn to YouTube (41%) and podcasts (20%) for information on financial products.

These statistics indicate that the traditional channels used by financial institutions to educate and inform their customers need the support of new and innovative ways to educate and engage younger demographics.

Digital Banking in the US

Digital banking has become an increasingly popular option in the US, especially among younger generations. Digital banking are banking services that are available online or through mobile apps, allowing customers to manage their finances on-the-go.

Digital banks in the US offer a range of financial products and services, including investment accounts, savings accounts, and retirement planning products.

Well-known benefits of digital banking include:

- Convenience

- Flexibility

- 24/7 access to the accounts

- Easily monitor portfolio

- Make trades on the go, without having to visit a physical bank.

Additionally, digital banks often have lower fees and higher interest rates on savings accounts, making them an attractive option for budgeting and saving.

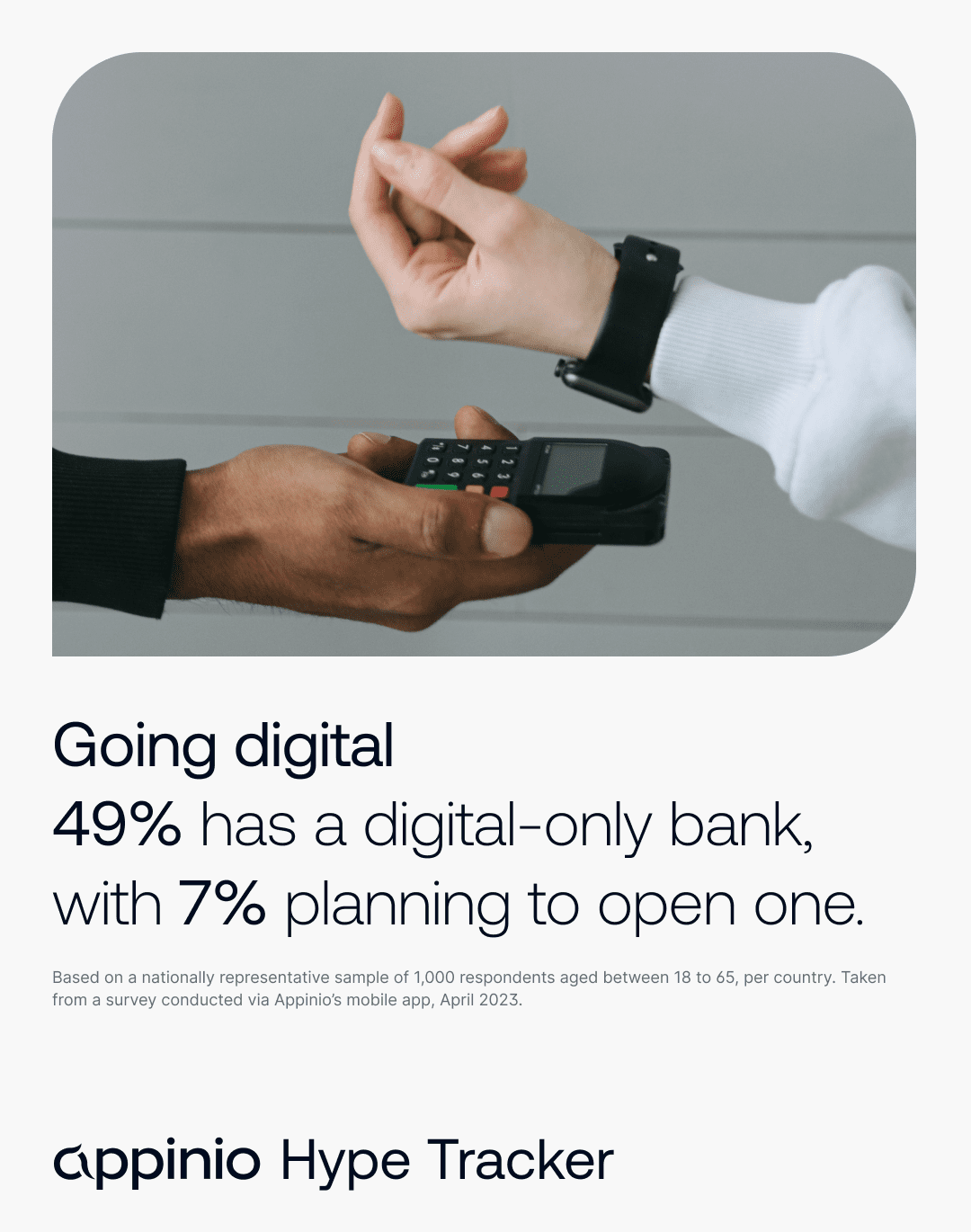

49% of Americans hold an account at a digital bank and 7% of them are planning to open one.

Reasons Americans are Switching to digital banks

Some of the most common reasons why US respondents have switched or are considering to switch to a digital bank were:- Attractive mobile / web app (49%)

- Better accessibility (49%)

- Easier to use when compared to traditional banks (48%)

- Better financial products (35%)

- Better direct purchasing options (e.g. crypto) via banking app (28%)

The most common reason for switching to a digital bank is the appeal of an attractive mobile or web app, followed closely by better accessibility. This suggests that consumers are drawn to digital banks because of the convenience and ease of use provided by their technology.

Additionally, a significant portion of respondents cited ease of use as a factor in their decision to switch to a digital bank. This could indicate that consumers find traditional banks to be more complicated and difficult to navigate, and that digital banks offer a simpler and more streamlined experience.

Interestingly, some consumers also cited better financial products as a reason for switching to a digital bank. This suggests that consumers are not only attracted to the technology provided by digital banks, but also to the financial services and products that these banks offer.

Finally, a smaller but still significant portion of respondents cited better direct purchasing options via banking apps as a factor in their decision to switch to a digital bank. This could indicate that digital banks are seen as more convenient and provide better variety and cost-effective product options compared to traditional banks.

There are many digital banks in the US, each with its own unique features and benefits. Some popular digital banks in the US include Ally Bank, Axos, Chime.

Americans’ trust in banks

Although digital-only bank account owners may attest to the product's value, the level of trust from the general public towards these banks is still lower than that for traditional banks.

81% of Americans trust traditional banks, while digital banks trail with 73% trust. But there is a way to win the hearts and loyalty of these detractors.

When asked what offers or features would make they switch, digital bank detractors listed the following ones:

- Lower / no fees 42%

- Cashback 33%

- Instant money transfers 26%

Overall, these statistics suggest that people are looking for tangible benefits when it comes to digital banking, such as cashback, lower fees, and instant money transfers.

Americans’ saving habits and goals

Savings are an essential component of personal finance, providing financial stability and a safety net for unexpected expenses.

As we’ve read before in this article, a savings account is a common financial product, 47% of Americans hold one.

It can be opened at banks or other financial institutions. It allows individuals to save their money and earn interest on the balance. Savings accounts are a low-risk investment option, making them ideal for people who want to protect their money while earning interest.

The Appinio Hype Tracker Report reveals two very interesting findings, which are:

- The majority of both American men and women have less than $50,000 in savings

- 67% of Americans are unable to put away more than $1000 a month.

But what are the things Americans are saving for? Let’s have a look at their saving goals.

Top saving goals among people in the US

- Emergencies

One quarter (23%) of Americans are saving for the unexpected — a sensible approach to financial planning. It’s always a good idea to have some savings set aside for unexpected expenses or job loss. 45-65 years-olds are the most likely to be saving in case of emergencies at 65%. - Retirement

Sharing a tied score with emergencies as a top savings goal, one quarter (23%) of Americans are currently saving for retirement. Men are more likely than women to save for retirement, 27% vs. 20%. This could be a positive sign, as it suggests that people are thinking ahead and taking steps to secure their financial futures. - No goals, just savings

19% are saving without a specific goal in mind. This could indicate that they have a general desire to build up their savings or create a financial safety net. 18-34 year-olds are the most likely to be saving money without any particular goals at 47%. - Item to buy (e.g. car)

17% of Americans are saving to buy items, such as cars or handbags. 25-44 year olds are the most likely to be saving for this purpose at 55%. - Holiday

17% are saving for a holiday. Americans are prioritizing experiences and making time for leisure in their lives. 25-44 year-olds are the most likely to be saving for this purpose (50%). - House

16% are saving to buy a house. Property ownership remains an important part of the American dream for many people in the US. This is a significant financial goal that requires a lot of planning and saving. Millennials are the most likely to be saving for this purpose (22%), followed closely by Gen Z at 20%. - Medical bills

14% of Americans are saving to cover costs of medical bills, with Gen Z leading the pack at 29%, followed by Millennials at 19%.

The Appinio Hype Tracker report highlights that a significant portion of Americans lack confidence in their financial readiness for the future, with 34% uncertain about saving enough for retirement and 33% feeling unprepared to start a business due to insufficient funds.

An additional 32% don’t feel confident they’ll be able to save enough to afford buying a rental property.

Conclusion for US Finances

Finance and personal finance are topics that affect everyone and are becoming increasingly important in our modern world.

The shift towards digital banking and the availability of various investment options have made it easier for people to manage their finances and grow their wealth.

However, it’s essential to understand the various financial products available, their benefits, and their risks and invest in increasing the levels of financial literacy.

This article, along with the latest Appinio Hype Tracker Report, has explored some of the most common types of investments, the reasons why people switch to digital banks, and what Americans are saving for. We hope it provides food for thought for the development of the next generation of financial products and services.

Want to run your own study?

Then take your market research efforts to the next level, sign up to Appinio for free and talk to us.